Can you picture your retirement? If you can envision those future years, you’d probably see a life full of activity and decades of health, happiness and prosperity. The problem with this picture is that the pleasure and comfort of your later years depend, in large part, on the actions you take today.

Today’s Planning Variables

Americans used to count on a pension plus Social Security to get them through their “golden years,” but times have changed. Nowadays, Social Security represents a little more than 30 percent of the aggregate income of Americans age 65 and older. Social Security benefits are less significant, and the sums are diminishing and the age you can begin receiving benefits is higher.

As you think about how much you’ll need for a comfortable retirement, you may be startled to learn the impact of inflation. At an average inflation rate of 3 percent, your cost of living would double every 24 years. Your annual income will need to increase each year during retirement in order to maintain your standard of living. You’ll also have to consider the likelihood of increased medical costs and health insurance as you grow older. For instance, the average nursing home now costs more than $87,000 a year, and it’s likely to continue increasing. With these variables comes the realization that the responsibility for providing the bulk of your retirement income rests with you.

Gaining An Edge: Personal Saving Is The Key

The aging workforce, and the rising uncertainty of Social Security, has increased the demand for retirement plans. Saving for retirement in a tax-efficient and low-cost investment program can accelerate your retirement savings. Also, investing in tax-efficient, non-retirement strategies involving real estate, stocks, and bonds can play a significant role in accumulating your nest egg.

Let’s Crunch The Numbers and Estimate How Much You Need!

While this is simplistic, try and follow the key concepts. Experts estimate you will need some 80 to 100 percent of your annual income each year in retirement. Find out how close you are to meeting this goal by completing the following exercise.

1. Estimate your future cost of living

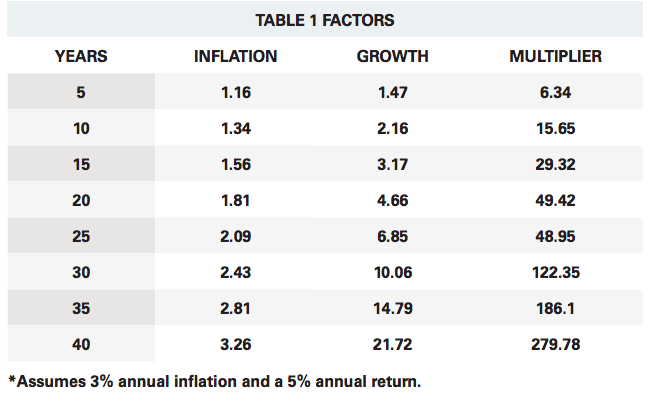

Multiply your current earnings by the inflation factor from figure one, based on the number of years you have until retirement.

Example: If you are currently making $100,000 and have 20 years until retirement, your formula is $100,000×1.81 = $181,000.

2. Determine the percenatge of your current income you may need after retirement

If 100 percent seems high, consider while you may be able to stop paying some expenses, like mortgage payments, other expenses may increase, such as health and travel expenses. Multiply that percentage by the amount in step one.

Example: $181,000 x .85 = $153,850. (85 percent of annual income)

3. Estimate your future Social Security and other pension retirement benefits

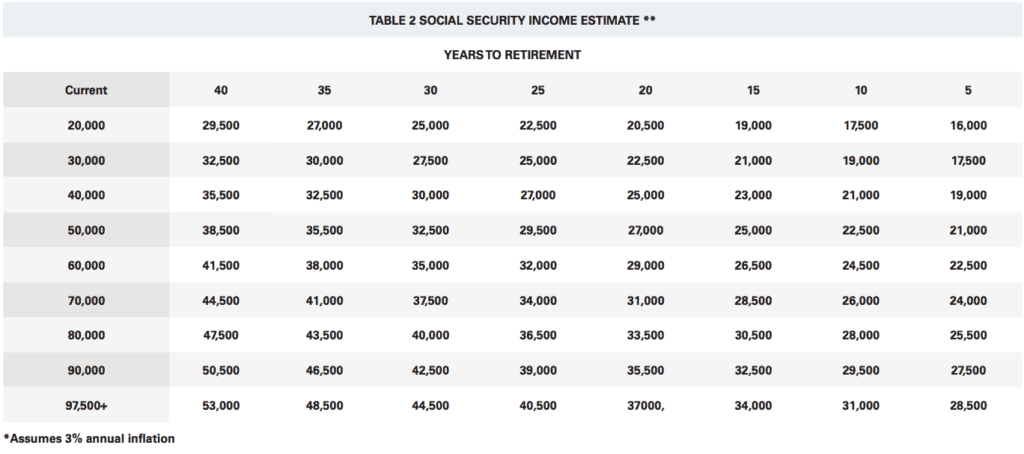

The best source for Social Security benefit projections is the Social Security Retirement Estimator at www.ssa.gov/estimator. (If you cannot access the official calculator, you can get a rough estimate of your benefit from figure two.)

If you are using figure two, take the number corresponding to your annual salary and years to retirement.

Example: With $100,000 in earnings and 20 years to retirement, your estimated benefit would be $37,000.

4. Calculate the net income you need to maintain your standard of living

Subtract your Social Security benefits and other retirement benefits from the annual amount calculated in step two. This will give you an estimate of how much of your own savings you will have to use each year in retirement.

Example: $153,850 – $37,000 = $116,850.

5. Estimate the total amount you will need to retire

Multiply 19.3 by the annual amount you calculated in step four. This represents how much savings you would need to last 30 years at 3 percent inflation and earning a 6 percent annual return.

Example: $116,850×19.3 = $2,255,205.

In this example, the goal is an estimated $2,255,205 for retirement.

If you are concerned about your retirement accumulation goals, take heart. You have some powerful allies on your side. First is the power of compounding, which takes advantage of time. Tax deferral is another ally. Use investment vehicles designed to put off paying taxes on your earnings until you are retired and potentially in a lower tax bracket. Meanwhile, your contributions may be pre-tax or tax deductible, helping reduce current tax bills.

If you need professional help, don’t underestimate the benefit of working with a qualified financial advisor. An expert can help you implement an investment program and monitor your progress. Having someone keep you accountable in working towards your goals is invaluable. Do not delay planning for your retirement.

For more information call AC Financial at 210.231.0456 or visit www.myacinvestments.com. AC Financial is located at 242 W. Sunset Road, Suite 101 in San Antonio, TX 78209.

Recent Comments